Macroscope

Quarterly Macro & Market Review

1Q 2024

By Sophie Metulescu

With the collaboration of Victoria Romero

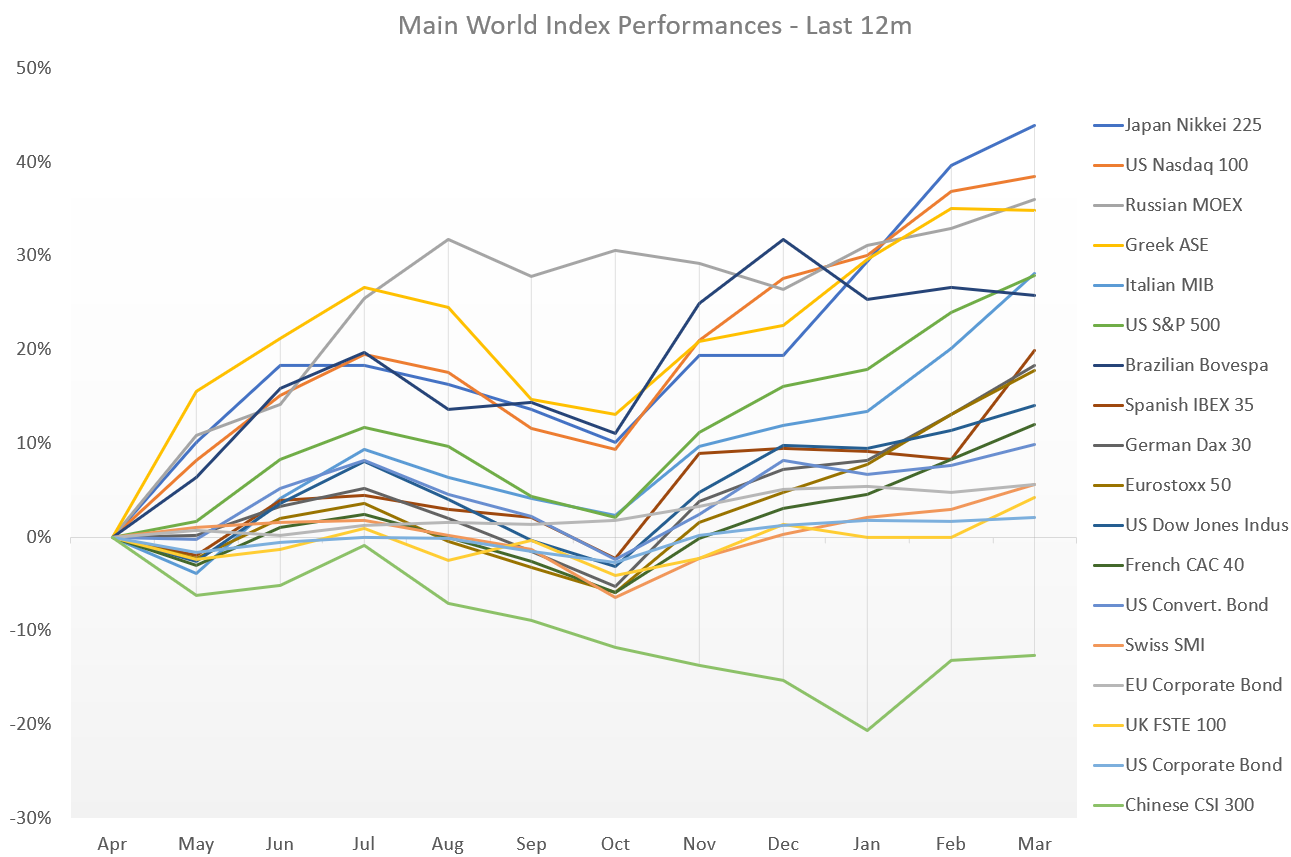

Market Performance

Data source: Bloomberg

Macroscope

Quarterly Macro & Market Review

1Q 2024

– EQUITIES

Global stock markets registered strong gains in Q1 amid a resilient US economy and ongoing enthusiasm around Artificial Intelligence. Expectations of interest rate cuts also boosted shares – although, as we know now, the pace of cuts is likely to be slower than the market had hoped for at the beginning of the year.

Sources: JP Morgan, Schröder, Bloomberg

In Europe

- Eurozone shares posted a strong gain in Q1.

- The information technology sector led the rally fueled by ongoing optimism over demand for AI-related technologies.

- The other strong sectors included financials, consumer discretionary and industrials, boosted by positive economic outlook while banks were supported by announcements of improvements in profits.

- By contrast, utilities, consumer staples and real estate were the main laggards.

In the US

-

US shares registered a robust quarter. Gains were supported by good corporate earnings as well as ongoing expectations of rate cuts later this year, nurrishing an appetite form risk and thus equities.

-

Gains were led by the communication services, energy, information technology and financials sectors.

-

Real estate registered a negative return while utilities also lagged.

In the UK

- UK equities rose over the quarter.

- Financials, industrials and the energy sector outperformed moved up by growing hopes in a sooner-than-expected first UK interest rate cut as inflation undershot the Bank of England’s forecasts.

In the Rest of the World

- The Japanese equity market experienced an exceptionally strong rally, with the Nikkei recording a Q1 return of 20% in Japanese yen terms. Foreign investors played a leading role in driving the upswing.

- Asia ex-Japan equities achieved modest gains for the period, with share prices bouncing back from recent lows as investors stayed cautious in the gloom surrounding China growth.

Macroscope

Quarterly Macro & Market Review

1Q 2024

REVIEW BY ASSET CLASS

– FIXED INCOME & FISCAL POLICIES

The bonds saw negative returns in Q1.

As the quarter progressed, governmental bond yields adjusted in response to shifting market sentiments and economic indicators. 10Y government bond yields increased across the board (meaning prices fell).

Corporate bonds still surpassed government bonds in performance. Convertible bonds did not fully benefit from the strong equity market tailwind advancing a shy 1.1%.

In Europe

- Eurozone inflation continued to cool down in Q1. The annual inflation rate (Consumer Price Index) was 2.6% in February, down from 2.8% in January, and remained unchanged in March.

- In February, European Central Bank President Christine Lagarde denied the chances of an imminent interest rate cut. She told the European Parliament that the central bank does not want to run the risk of reversing any cuts by doing it too soon and seeing as a result the inflation coming back.

In the US

- The US economy continued to outperform, buoyed by sustained consumer spending, thanks to rising real wages and easing inflation.

-

The Fed kept interest rates on hold at 5.25-5.5%. Fed chair Jerome Powell said that the central bank will be “careful” about the decision on when to cut rates. The latest “dot plot” that details policymakers’ expectations of rate cuts suggests three cuts this year.

In the UK

-

At the end of the period the BoE decided at its March meeting to keep the UK’s main policy interest rate on hold at 5.25%. Annual inflation, as measured by the consumer price index, has fallen from a peak of 11.1% in October 2022 to 3.2% in March, the lowest rate of price increases since September 2021.

-

Official data showed that the economy had entered a technical recession in the second half of 2023. This occurred as the tailwind of post-pandemic “revenge spending” came to an end and the headwinds of higher inflation and interest rates weighed on activity.

In the Rest of the World

- The Bank of Japan increased interest rates from -0.1% to 0.1% for the first time in 17 years, signalling an end to negative rates.

- The Swiss National Bank surprised the markets with a 25 basis point cut to 1.5% in March.

Macroscope

Quarterly Macro & Market Review

1Q 2024

REVIEW BY ASSET CLASS

– CURRENCIES: Fiat & Digital

- After a slow January, digital asset markets took off in February and March resulting in one of the strongest quarters in recent history. Bitcoin and Ethereum returned 68.8% and 59.9%, respectively. Bitcoin reached a new all-time high on 14 March.

- These strong returns were generated by a high demand following the approval and launch of eleven physically backed Bitcoin ETFs (exchange traded funds) in the US on 11 January. These products have reveived net inflows of $12.1 billion since inception. Market dynamics have also seen a step-change since last quarter, with Bitcoin trading volumes up 85% year-to-date.

- The USD gained quite signficantly (+7%) against CHF and JPY helped by the “higher for longer” rate policy.

Macroscope

Quarterly Macro & Market Review

1Q 2024

REVIEW BY ASSET CLASS

– COMMODITIES

- The S&P GSCI Index achieved robust growth in the first quarter, with all components of the index ending the period in positive territory: Energy and livestock were the best-performing components, while agriculture and industrial metals achieved more modest growth.

- Within energy, all sub-sectors achieved strong price growth apart from natural gas, which experienced a sharp price fall in the quarter.

-

Within agriculture, the price of cocoa rocketed higher due to strong demand and shortages in West Africa, where more than half of the world’s cocoa beans are harvested.

-

In industrial metals, zinc and aluminium prices fell, while prices for copper, lead and nickel were modestly higher. Both gold and silver prices also advanced in Q1.

Macroscope

Quarterly Macro & Market Review

1Q 2024

THIS QUARTER IN THE LIMELIGHT

– News & Buzz

Macroscope

Quarterly Macro & Market Review

1Q 2024

IN THE FUTURE

– WHAT THE SPECIALISTS SEE FOR 2024

Clare Lombardelli, OECD Chief Economist

“Governments need to start confronting the mounting challenges that public finances face, particularly from ageing populations and climate change.”

Remi Olu-Pitan, Head of Multi-Asset Growth & Income, Schröder

“The US was the only game in town, but not anymore and the Bank of Japan maintaining negative real yields, despite raising interest rates, really highlights this. ”

Xavier Baraton, Global Chief Investment, HSBC

“Current market pricing remains consistent with a soft-landing scenario, seemingly overlooking the elevated risk of recession. Our ‘house view’ is defensive: Bonds are back.“

Jamie Dimon, CEO, JP Morgan Chase

“There is a growing need for increased spending as we continue transitioning to a greener economy, restructuring global supply chains, boosting military expenditure and battling rising health care costs.”

Wei Li, Global Chief Investment Strategist, BlackRock

“Expectations for S&P 500 earnings growth for 2024 have been revised up, with the tech sector expected to account for half of this year’s S&P 500 earnings.”

Macroscope

Quarterly Macro & Market Review

1Q 2024

FINANCIAL BUZZ

– THE NEW TERM TO MASTER TODAY

Bitcoin Halving

“With bitcoin’s price hitting new record highs, the crypto world is bracing for the next “bitcoin halving” on April 19, an event that occurs every four years. We break down what is bitcoin, how it works and what the halving means for investors.”

Macroscope

Quarterly Macro & Market Review

1Q 2024

THE QUARTER AHEAD

– MAIN EVENTS & WHAT TO EXPECT

17-19 Apr: The Spring Meetings of the IMF and WBG 2024

The Spring Meetings are held jointly by the IMF and the World Bank in Washington, D.C.. This event will bring together private sector executives, central bankers and ministers of finance to discuss issues of global concern and economic outlook.

What we can expect:

The main topics will be about Middle East tensions and inflation issues.

30-01 Apr/May: FOMC Meetings

The FOMC (Federal Open Market Committee) is the branch of the Federal Reserve that determines the direction of monetary policy of the United States.

What we can expect:

According to the latest economic inflation data, consensus thinks the Fed is likely to cut interest rates at least once in 2024, with the largest share of officials expecting three cuts. The timing and frequency of rate cuts will depend on a variety of factors, including inflation and the labor market.

06-08 May: Industry Strategy Meeting, New York

This in-person meeting will gather chief strategy officers from industry communities, senior representatives from government, academia, civil society and the World Economic Forum Innovators communities under the theme “Shaping Business Transformation in an Era of Disruption”.

What we can expect:

The meeting will draw the lessons and takeaways of the World Economic Forum Annual Meeting 2024 and prepare the road-map to strategic impact solutions.

22 May: The ECB Governing Council retreat in Ireland

The Governing Council is the main decision-making body of the ECB. They draw the guidelines and are the ones that formulate monetary policy for the euro area. This year the Retreat is hosted by the Central Bank of Ireland.

What we can expect:

ECB policymakers will discuss green monetary policy and their upcoming strategy review, where they will also pave the ground for a likely interest rate cut in June.